All Categories

Featured

Table of Contents

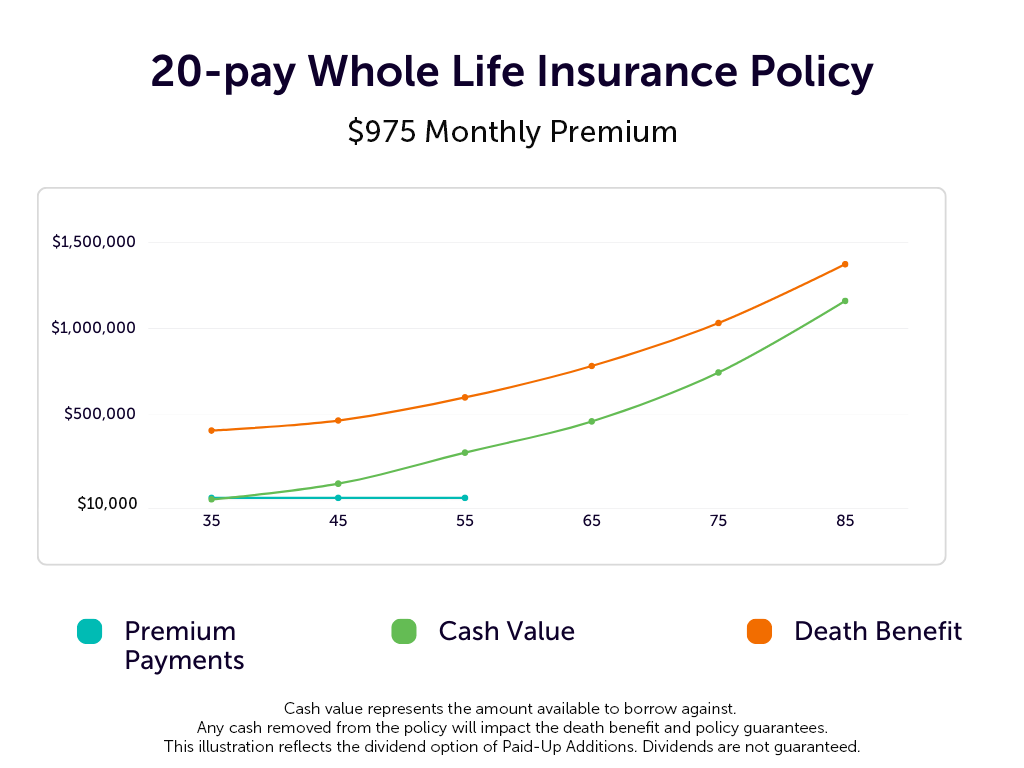

For most individuals, the greatest trouble with the limitless banking principle is that first hit to very early liquidity caused by the costs. Although this disadvantage of unlimited banking can be decreased significantly with proper policy style, the first years will constantly be the most awful years with any Whole Life policy.

That claimed, there are certain boundless banking life insurance policy policies created largely for high very early cash worth (HECV) of over 90% in the first year. Nonetheless, the long-term performance will certainly commonly considerably delay the best-performing Infinite Banking life insurance coverage policies. Having access to that additional four numbers in the first few years might come at the cost of 6-figures later on.

You really obtain some substantial long-lasting advantages that aid you recoup these early costs and then some. We locate that this impeded early liquidity trouble with boundless financial is a lot more mental than anything else once extensively checked out. If they definitely needed every dime of the money missing from their boundless financial life insurance policy in the very first few years.

Tag: boundless banking concept In this episode, I speak regarding funds with Mary Jo Irmen that instructs the Infinite Financial Principle. With the surge of TikTok as an information-sharing system, financial guidance and strategies have actually discovered a novel method of spreading. One such approach that has been making the rounds is the unlimited financial idea, or IBC for short, amassing endorsements from celebrities like rapper Waka Flocka Flame.

Within these plans, the cash worth expands based on a price established by the insurance provider. When a considerable cash money value accumulates, insurance policy holders can acquire a cash money worth finance. These finances vary from standard ones, with life insurance policy working as security, indicating one could shed their protection if loaning exceedingly without adequate cash money value to support the insurance expenses.

And while the allure of these plans is obvious, there are inherent constraints and threats, necessitating thorough money value tracking. The technique's authenticity isn't black and white. For high-net-worth individuals or local business owner, specifically those utilizing approaches like company-owned life insurance (COLI), the benefits of tax obligation breaks and compound development can be appealing.

Nelson Nash Scam

The allure of unlimited financial does not negate its difficulties: Cost: The fundamental requirement, a long-term life insurance plan, is more expensive than its term counterparts. Eligibility: Not everybody gets whole life insurance policy as a result of extensive underwriting procedures that can omit those with details wellness or lifestyle conditions. Complexity and danger: The complex nature of IBC, coupled with its dangers, may discourage several, especially when simpler and less dangerous choices are offered.

Assigning around 10% of your regular monthly earnings to the policy is simply not viable for many individuals. Component of what you check out below is just a reiteration of what has currently been said over.

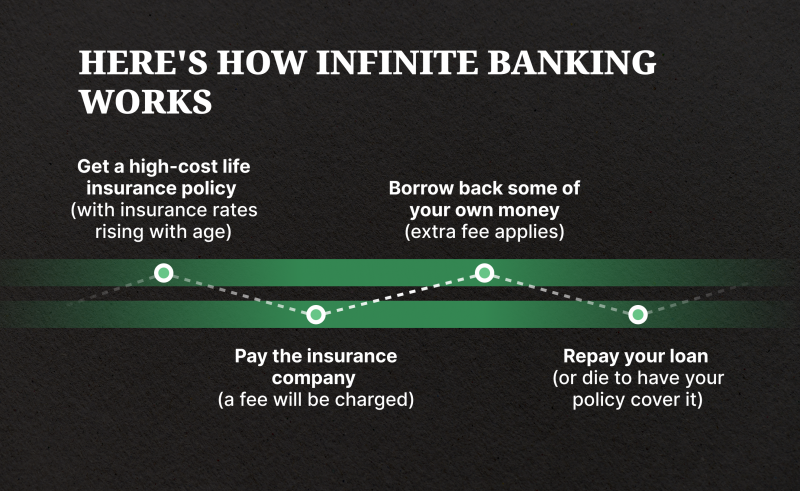

So before you get on your own right into a scenario you're not planned for, recognize the complying with initially: Although the idea is frequently marketed as such, you're not really taking a lending from on your own. If that were the instance, you would not have to settle it. Instead, you're obtaining from the insurance provider and have to settle it with passion.

Some social media messages advise using money value from entire life insurance policy to pay for bank card financial debt. The concept is that when you pay back the finance with rate of interest, the amount will certainly be sent back to your financial investments. That's not just how it functions. When you pay back the car loan, a section of that rate of interest mosts likely to the insurer.

For the initial several years, you'll be settling the commission. This makes it very hard for your plan to build up worth during this time. Whole life insurance costs 5 to 15 times more than term insurance. Many people just can not afford it. Unless you can pay for to pay a couple of to numerous hundred bucks for the next years or more, IBC won't work for you.

Infinite Banking Concept Book

If you call for life insurance, below are some valuable tips to take into consideration: Consider term life insurance policy. Make sure to shop about for the finest rate.

Copyright (c) 2023, Intercom, Inc. () with Scheduled Typeface Call "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Reserved Font Style Call "Montserrat".

How Infinite Banking Works

As a CPA concentrating on property investing, I have actually brushed shoulders with the "Infinite Financial Idea" (IBC) a lot more times than I can count. I've even spoken with professionals on the subject. The primary draw, besides the apparent life insurance policy benefits, was always the concept of accumulating cash money value within a permanent life insurance policy and loaning against it.

Sure, that makes sense. However honestly, I always thought that cash would be better invested directly on investments rather than funneling it with a life insurance policy policy Up until I found how IBC can be combined with an Irrevocable Life Insurance Policy Count On (ILIT) to produce generational riches. Allow's start with the basics.

Synchrony Bank Infinite Credit Card

When you obtain against your plan's money worth, there's no set repayment schedule, giving you the liberty to take care of the financing on your terms. The money value continues to expand based on the policy's assurances and dividends. This configuration permits you to accessibility liquidity without interrupting the long-lasting development of your plan, gave that the loan and rate of interest are taken care of carefully.

As grandchildren are born and grow up, the ILIT can purchase life insurance plans on their lives. Household participants can take financings from the ILIT, using the money value of the policies to fund financial investments, start services, or cover significant costs.

A crucial facet of managing this Family Financial institution is the use of the HEMS criterion, which represents "Health, Education And Learning, Upkeep, or Assistance." This guideline is frequently consisted of in count on contracts to route the trustee on how they can distribute funds to beneficiaries. By sticking to the HEMS requirement, the trust fund guarantees that circulations are made for essential needs and long-term support, protecting the depend on's properties while still offering for member of the family.

Enhanced Flexibility: Unlike rigid financial institution fundings, you control the repayment terms when borrowing from your own policy. This enables you to structure settlements in such a way that aligns with your business cash money circulation. what is infinite banking life insurance. Enhanced Money Flow: By financing service expenditures through plan finances, you can possibly maximize money that would certainly otherwise be tied up in typical lending settlements or tools leases

He has the same devices, yet has actually also developed additional cash money worth in his plan and obtained tax obligation benefits. And also, he now has $50,000 available in his plan to make use of for future possibilities or costs., it's important to see it as more than just life insurance coverage.

Infinite Banking Insurance Policy

It's about producing a versatile funding system that gives you control and gives several benefits. When made use of strategically, it can complement various other investments and service strategies. If you're interested by the potential of the Infinite Banking Concept for your business, below are some actions to take into consideration: Educate Yourself: Dive deeper into the concept through reputable publications, workshops, or assessments with knowledgeable specialists.

{kind=link}

Latest Posts

How To Start Your Own Private Bank?

Nelson Nash Becoming Your Own Banker Pdf

Infinite Banking Concept Calculator